Table of Contents

STP Phase 2 - Employer Checklist of key changes

The following article is a checklist that employers can refer to in order to assist Reckon Accounts users in obtaining or preparing the required information ahead of time for Single Touch Payroll (STP) Phase 2.

Key changes:

- Are you a Registered Employer for Working Holiday Makers?

- Have you changed your payroll solution during a financial year?

- What Tax Category do my employees belong to?

- What is the Home Country of my employee under Working Holiday Maker program?

- What is your employee's Medicare Levy obligation?

- Does your Voluntary Agreement employee use the Commissioner's Instalment Rate?

- Changes for Payroll Items

Company Information

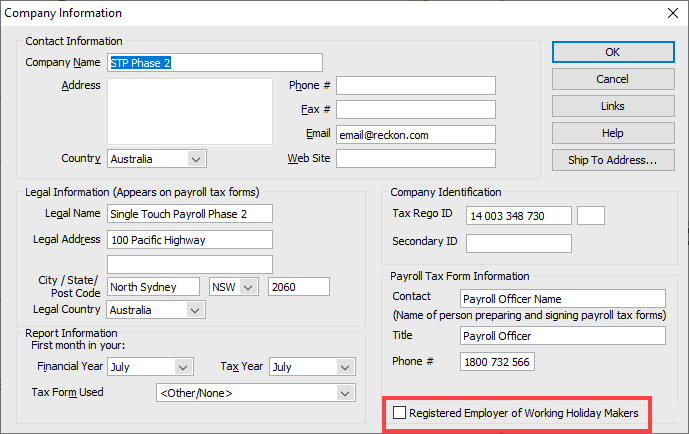

Are you a Registered Employer for Working Holiday Makers?

Working Holiday Makers (WHM) are temporary visitors to Australia.

If you employ or plan to employ a WHM who holds a Working Holiday visa (subclass 417) or Work and Holiday visa (subclass 462), you need to register with the ATO as an employer of working holiday makers.

To identify if the business is registered or unregistered we have added a checkbox in Reckon Accounts 2023. This option will not affect any calculations, but it will be used to create the Tax Treatment Code for your employee that is reported in each STP event.

Have you changed your payroll solution during a financial year?

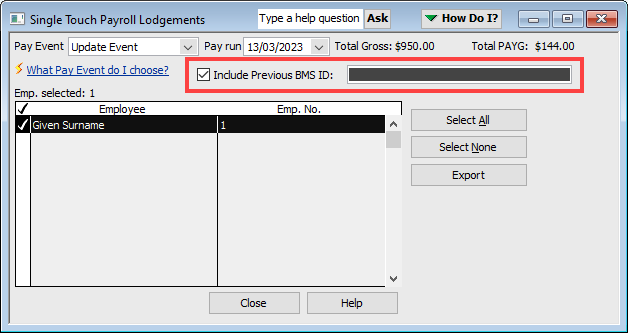

Any compliant STP-enabled payroll solution has a BMS ID (Business Management Software Identifier) that is either assigned, generated, or user-nominated. This helps the ATO identify the source of employee data or payroll solution used when an STP report is sent out.

There are a number of options to inform ATO of the changes that can be referred from Changing your payroll solution or employees’ Payroll IDs during a financial year.

The Previous BMS ID would only need to be reported to the ATO once after the change during an Update Event.

Employee

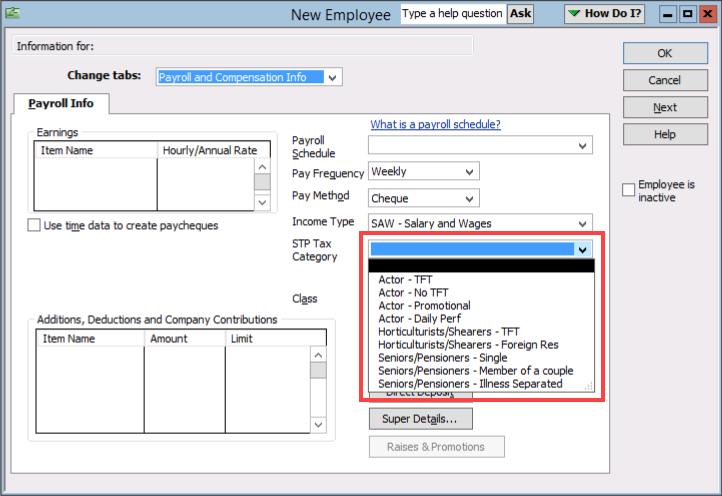

What Tax Category does my employee belong to?

The STP Tax Category fields does not affect any payroll calculation and are used for STP Phase 2 reporting purposes only. Therefore, continue to use the relevant Tax Code for each employee.

For example, an STP Tax Category: Actor – TFT does not require you to change your Tax Code to

2-TFT. If no Tax scale is appropriate, use 8-No TaxC and enter the correct Tax Rate.There are a number of components that influence the rate of withholding a payer applies to the payees’ payments that are subject to withholding. The STP Tax Category is one of the factors for the Tax Treatment Code that identifies the payee setup for the calculation of the PAYGW and their circumstances to the payer.

In Reckon Accounts, the available Tax Categories are:

INCOME TYPE | STP TAX CATEGORY |

|

|

|

|

|

|

|

|

— Income Type: Reporting the amounts you have paid | Australian Taxation Office (ato.gov.au)

— STP Tax Category: Tax treatment section on How to report employment and taxation information through STP Phase 2 | Australian Taxation Office (ato.gov.au)

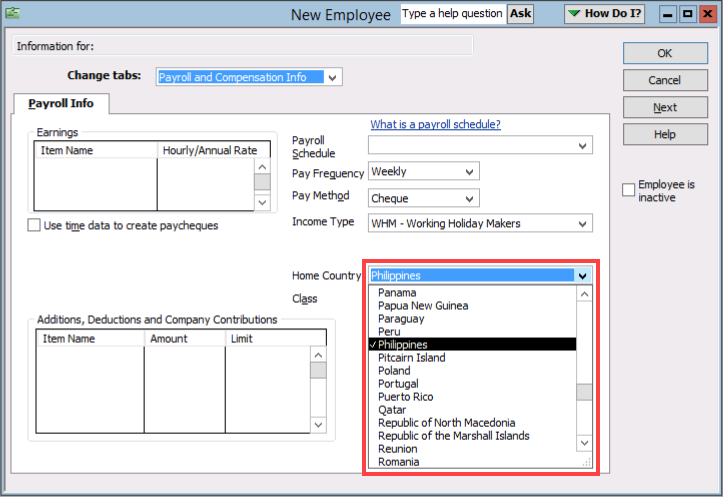

What is the Home Country of your employee under the WHM program?

When your employee is under the Working Holiday Maker program the ATO requires the Home Country of the worker to be reported. The Home Country dropdown will be enabled when the Income Type is set to Working Holiday Maker.

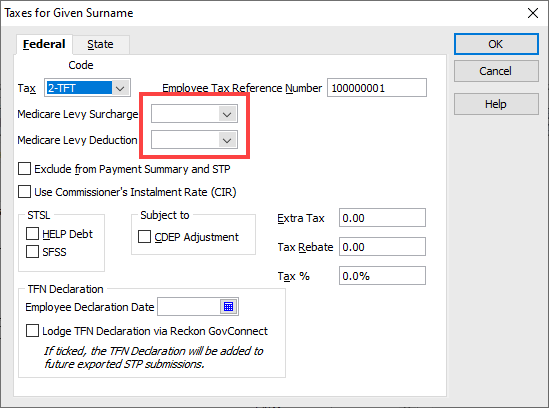

What is your employee's Medicare Levy obligation?

Do not select anything if you do not need to claim. To check if you qualify, check with your health care provider, your accountant, or with the ATO.

The Medicare Levy is an amount paid in addition to the tax paid on the employee's taxable income. This helps fund the national health system, Medicare, and calculated at 2% of your taxable income.

Based on the employee's income, a Medicare Levy Surcharge may be required. This is an additional payment on top of the Medicare Levy. An employee may be exempt or are able to reduce their Medicare Levy depending on their circumstances:

- A Medicare Levy Exemption is a payment exemption for the entire or part of the year for the Medicare Levy.

- The Medicare Levy Reduction helps reduce the Medicare Levy an employee has to pay if eligible.

Generally:

- When a Medicare Levy Surcharge is applied, an employee cannot apply exemptions and reductions.

- When a Full Medicare Levy Exemption is applied, an employee cannot apply surcharge and reduction.

- If Half Medicare Levy Exemption is applied, an employee cannot apply the surcharge, however a reduction will be available.

- When a Medicare Levy Reduction is applied, the employee cannot apply the surcharge, however, half exemption will be available.

- A Single Senior or Pensioner cannot apply for Medicare Levy Reduction as they have no Spouse.

5-Full ML or 6-Half MLMEDICARE LEVY SURCHARGE | MEDICARE EXEMPTIONS | MEDICARE LEVY REDUCTION |

|

|

|

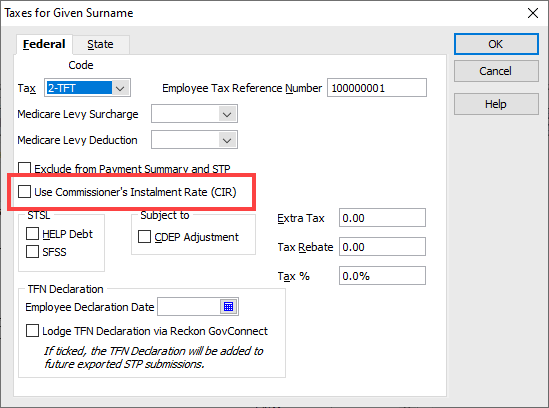

Does your Voluntary Agreement employee use the Commissioner's Instalment Rate?

A Voluntary Agreement is a written agreement between a payer and a contractor payee to bring work payments into the PAYGW system. The payer does not have to withhold amounts for payments they make to contractors.

However, the payer and a contract worker (payee) can enter into a voluntary agreement to withhold an amount of tax from each payment they make to the contractor. This can be the contractor's PAYG instalment rate, called the Commissioner's instalment rate (CIR) or a flat rate of 20%.

In Reckon Accounts, a business can notify the ATO if an employee is under the Income Type: Voluntary Agreement and using a CIR by going to the Taxes window and checking the "Use Commissioner's Instalment Rate (CIR)" checkbox.

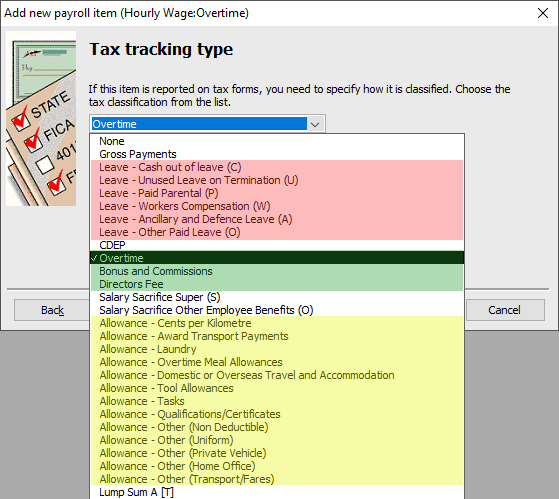

Changes to Payroll Items

Disaggregation of Gross

Gross payments

The Gross amount reported via STP consists of a total of many components and payment types. For this reason, the ATO has now expanded STP Phase 2 to report the Gross payments in more detail. Instead of reporting a single gross amount, employers will need to report the sources separately.

In Reckon Accounts, these are handled by assigning the Payroll Items to the correct Tax Tracking Type.

GROSS | ALLOWANCES | PAID LEAVE |

|

|

|

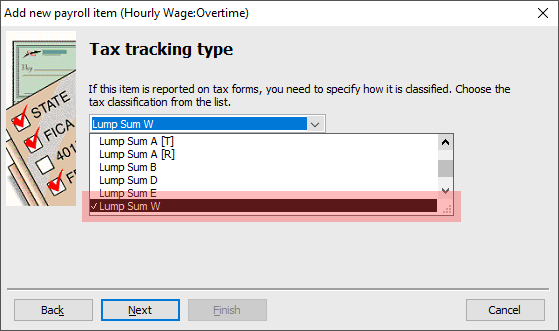

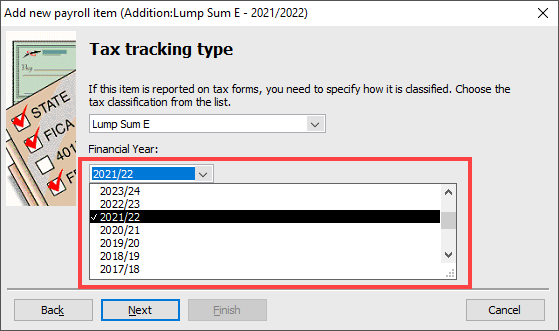

Lump sum payments

There are two changes with Lump Sum payments:

- The introduction of a new Category: Lump Sum W to report on 'Return to Work Payments'

- Each Financial Year relevant to the Lump Sum E payment must be reported

The Lump Sum W is available as a Tax Tracking Type in Reckon Accounts.

The Financial Year can now be set for Lump Sum E in the Payroll Item window.

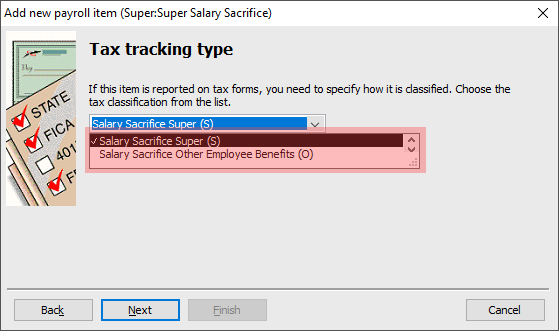

Salary sacrifice

Salary Sacrifice arrangements are now required to be reported separately.

To accommodate this, a new Tax Tracking Type can now be set for Super Payroll Items in Reckon Accounts.

- Salary Sacrifice from Super to a complying fund or Retirement Savings Account (RSA)

- Salary Sacrifice from Other Employee Benefits

Need more help?

Ask the Reckon Community at: https://community.reckon.com/categories/reckonaccounts

Or Log a Support Ticket: https://www.reckon.com/au/support/